Blockchain is a geeky, technical, but highly misunderstood term. If you have been hearing this term being thrown around along with web 3.0 and crypto, but are not exactly sure of what it is, this is the perfect blockchain for dummies article. Read on to find out what blockchain technology is and how does it work in simple terms, what its key features, benefits, and disadvantages are, and some real world examples.

What is Blockchain Technology in simple terms?

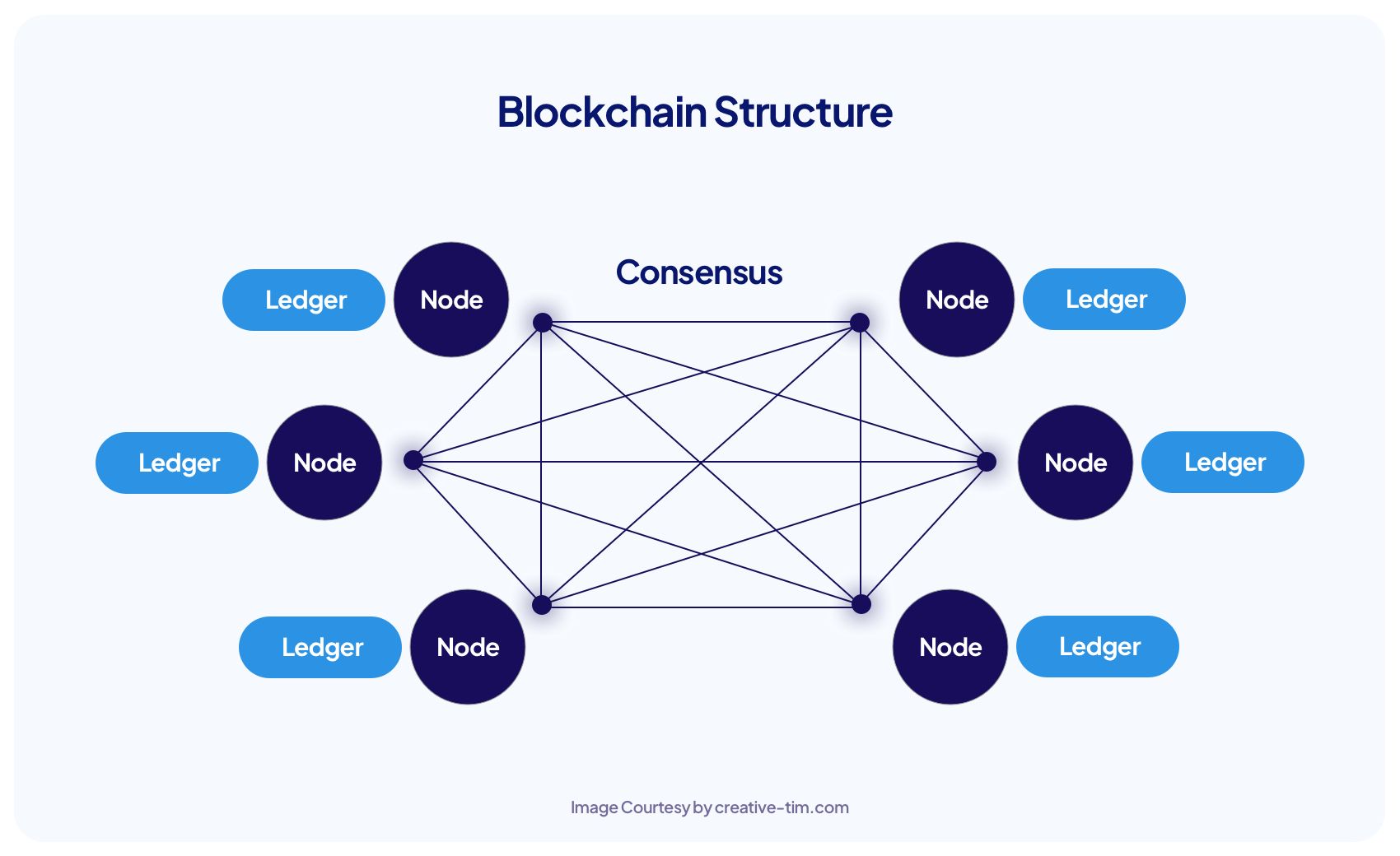

In the simplest terms, a blockchain is a computer file for storing data and that data which is contained within the blockchain is distributed (duplicated) across many computers (decentralised).

In more detailed and technical terms, the blockchain relies on peer-to-peer network technology, whereby the entire system is composed of peers (or nodes). Each peer in the network approves and records each transaction that takes place in the network. What this means is, that whenever a new transaction is added to the network, it is verified and added to each peer's ledger. This decentralized way of recording transactions in a ledger is called Distributed Ledger Technology (DLT).

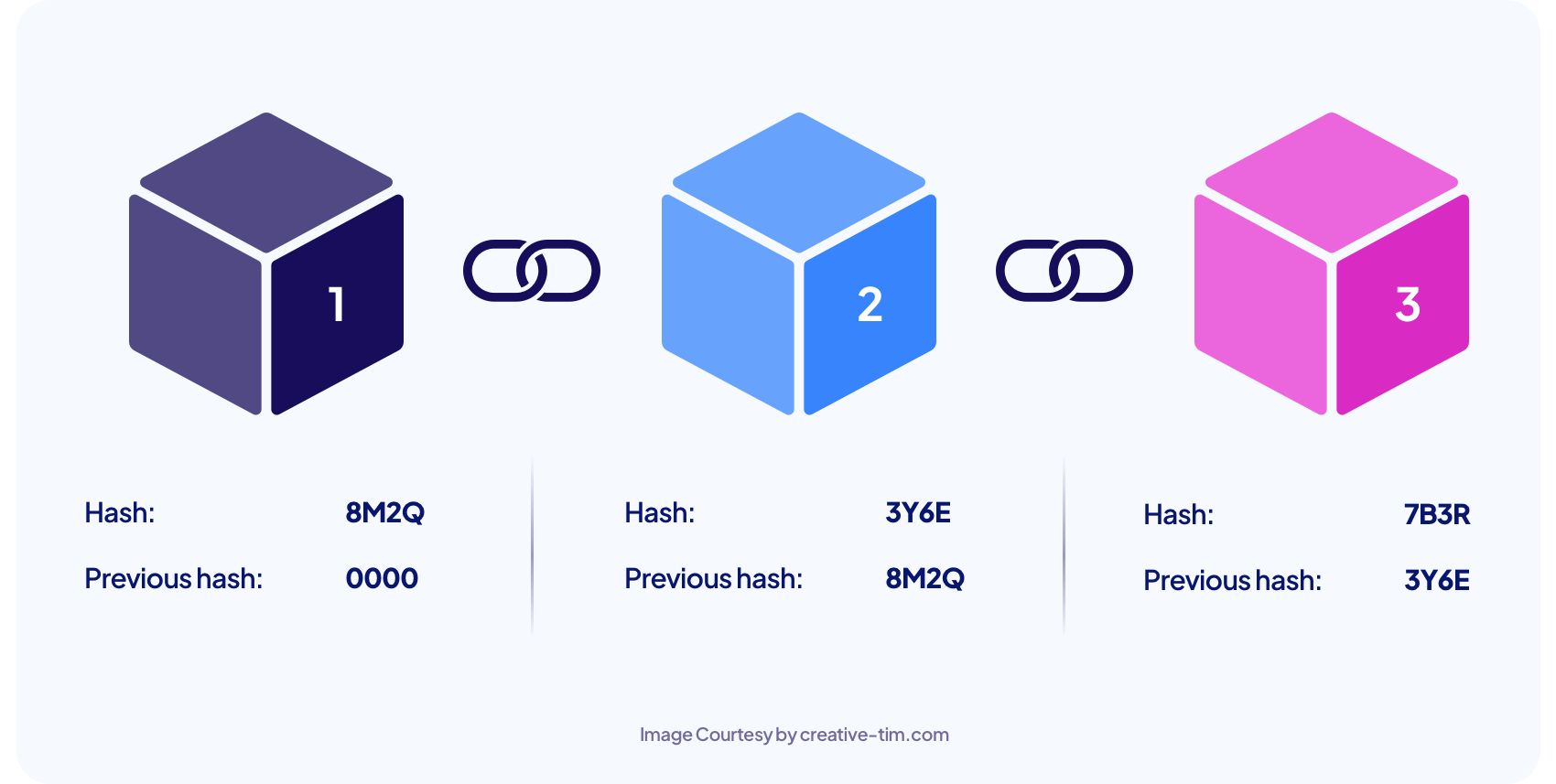

Blockchain is a type of DLT. Each transaction stored in the blockchain is called a block. Each block is chained to the previous block using a cryptographic hash. So, if someone wants to tamper with a certain block, they have to tamper with all the previous blocks in the chain, which is impossible/ extremely difficult since all peers have the same ledger, and any change is noticeable. This creates an immutable record of blocks, that does not require an external authority.

Hence, in the simplest terms, a blockchain is a chain of blocks. It is a process or technology of recording information as blocks that makes it impossible to change, hack, or cheat.

Resource: What is Web 3.0? Everything explained

What are the Key Features of a Blockchain?

Before actually understanding the working behind a blockchain, there are some key features you should understand:

Immutability

Immutability means that the blockchain is permanent. Once a block is created, it cannot be altered.

Distribution

All peers (or nodes) in the blockchain network are distributed and have a copy of the current ledger for transparency. A public ledger provides complete information about the participants available in the network, and the current ledger. In a distributed ledger:

- all changes are updated in minutes or seconds after verification

- no node is more special than the other since there is a standard protocol for adding blocks to a network.

Decentralization

Since there is no central authority that governs the operation of the distributed ledger, a blockchain network is decentralized. There is no third party involved, the network is less prone to failure, and does not depend on human calculations but rather on computing power.

Consensus

To make unbiased decisions, a blockchain network has a consensus. A consensus is a decision-making algorithm. Hence, even though peers do not trust each other, there is mutual trust in the consensus that can make decisions for the network.

Unanimity

All peers in the blockchain network must agree to add a block to the network. Hence, if a peer wants to add a block to the network, it must get majority voting. Once there is a unanimous decision to add the block, the block is added and the ledger is updated across every peer of the network.

Fast Settlement

Since blockchain uses consensus algorithms, computing power, unanimity, and decentralization for making decisions, blockchains usually reach a faster settlement than traditional centralized systems.

How does Blockchain Technology work?

The steps of adding a block to a blockchain network can be summarized in the following:

- A peer creates a new blockchain transaction using its computing power.

- The transaction is shared with all peers in the blockchain platform.

- All peers compute equations, validate the blockchain transaction, and can use consensus algorithms to come to a decision.

- Peers unanimously vote for the transaction to be included in a block.

- One block can cluster different transactions until it is full.

- A unique identifier containing a cryptographic hash of the current block, and the hash of the previous block is applied to the block.

- The block is added to the chain, and the ledger is updated across all peers.

The process of adding blocks to a blockchain network is called blockchain mining.

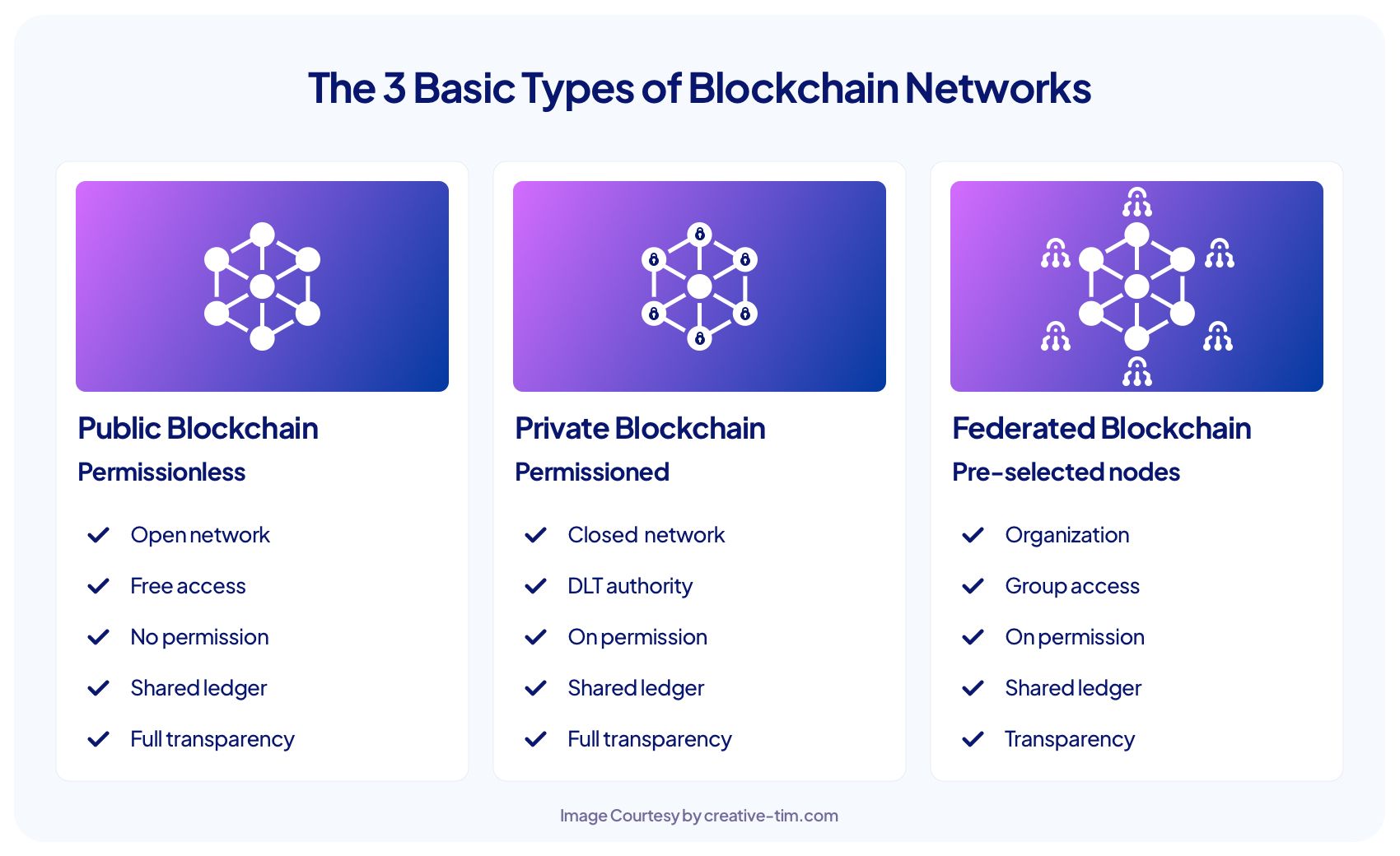

What are the Types of Blockchain Networks?

The underlying blockchain platform is further divided into the following blockchain networks depending on the permissions of each peer in the network:

- Public Blockchain Network

A public blockchain network also called a permission-less network, allows any peer to participate in the blockchain mining process without restrictions. The peers must however abide by the consensus algorithms.

- Private Blockchain Network

A private blockchain network also called a permissioned network, allows organizations to control the permissions of their peers. In other words, organizations can decide who can participate in blockchain mining, and who cannot. Access control is also applied to allow some peers to access specific sets of data.

- Federated Blockchain Network

A federated blockchain network, also called a consortium blockchain, is a network where the consensus algorithm is controlled by a preselected set of nodes. In other words, the blockchain mining process is governed by a pre-selected group of stakeholders.

Resource:Web 1.0 vs Web 2.0 vs Web 3.0. What are the differences?

How does Blockchain Security work?

Three aspects make the blockchain platform secure:

- Validation from all peers: All blocks in a blockchain must first be validated by all peers in the network before it is added to the ledger. This decentralized process in itself is a fool-proof mechanism to ensure that nobody can tamper with the data in a single peer, as the actual ledger is distributed across all other peers remaining in the network, and the discrepancy can be caught out upfront. Hence, in other terms, a blockchain network does not have a single point of failure.

- Individual encryption: Additionally, blocks in a blockchain are encrypted individually to provide an extra layer of security. The form of encryption applied is a cryptographic hash, which means that each block has its own identity. All peers in the network have private keys to solve the block's cryptographic hash. This means that if a hash is altered, the private key becomes invalid, and the peer network will know of the alteration immediately. This early notification prevents further damage.

- Chained to the previous block: Each block does not only have its hash, but also the hash of the previous block, so they are chained. Any attempt to modify one block means that the hash of all the blocks needs to be changed, which is an impossible thing as the computing power required to do so is massive.

How did Blockchain Technology evolve?

While blockchain was first envisioned by Stuart Haber and W. Scott Stornetta in 1991, Satoshi Nakamoto (who created Bitcoin, a cryptocurrency that is based on the blockchain platform) is attributed to be the brains behind the technology. Haber and Stornetta created a cryptographically secure chain of blocks and later upgraded their system in 1992 to incorporate Merkle Trees. However, blockchain became mainstream on 2009, when Nakamoto (who is anonymous) released the whitepaper about the technology and handed over the reins of Bitcoin to core developers.

Once Bitcoin became mainstream, blockchain started being used for transactions around 2012-2014. From 2014-2016, it saw its use in smart contracts, and now it is increasingly being used to create computer applications especially in the crypto world.

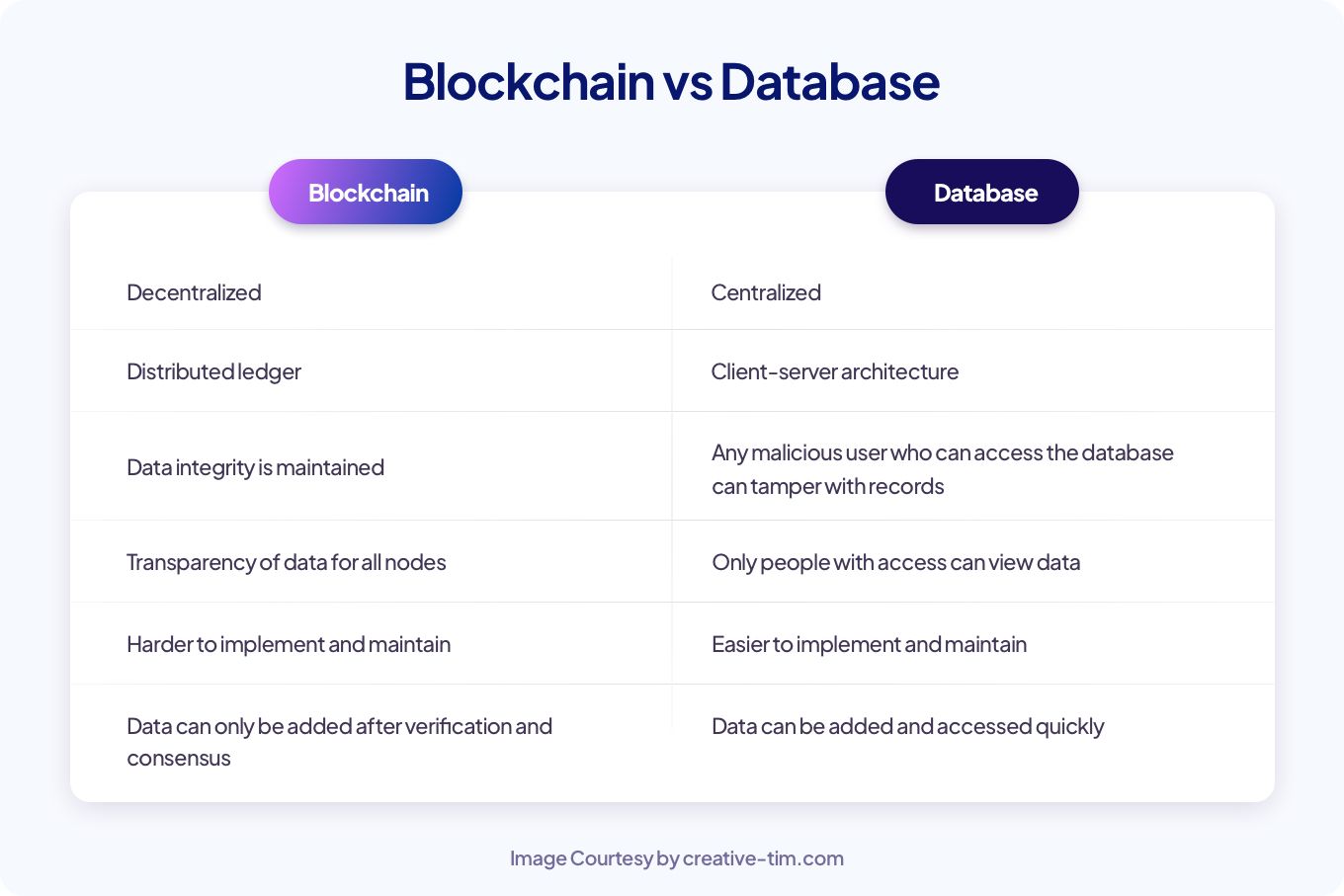

What is the difference between a Database and a Blockchain?

A database is a group of records, that exists on a ledger, and is run by an administrator. Only people with access to a database can read or write it. This definition itself outlines the differences that exist between a database and a blockchain:

What problems does Blockchain technology solve?

While understanding blockchain for dummies is easy, understanding the real-world reasons behind why blockchain is popular, is equally important. Blockchain isn't just a heavy terminology, but has some real-world applications that are making it extremely popular:

Data Retention

The data management offered by blockchains, whereby data is stored in all peers, is far superior to just storing critical data in a central location, which can be a single point of failure.

Government Operations

With a mix of biometrics and blockchain, critical government operations can be improved to offer better identity management systems. For example, blockchains can be used to verify tax records, thus making taxation systems more efficient.

Crowdfunding

Blockchain also finds its use in the crowdfunding of different projects. Blockchain technology ensures that transactions are anonymous, safe, and borderless, making finances accessible, secure and transparent. Thus, it can encompass global crowdfunding for just about anything.

Intellectual Property

If you create a digital trail of blocks or records for your intellectual property, which can be a song or a trade secret, you can copyright or protect your intellectual property using blockchain.

Data Protection

Since blockchains are secure by design, storing critical cloud data in distributed ledgers instead of centralized storage facilities can vastly improve data protection.

Voting

Using blockchain networks for voting can allow governments to safeguard voter identity, and each vote can be encrypted and saved to the blockchain, making it impossible to hack or modify. This in turn can truly phase out election manipulation.

Supply Chains

Yet another blockchain example that makes life easier is its use in supply chains. It can improve the process of supply chain product registration, connection, sharing, assignment, and tracking if every product's supply chain journey is documented using blockchains. This can, in turn, reduce the illegal and immoral transfer of assets.

Bypassing Intermediaries

Since blockchain is a network of peers, it allows transactions to bypass intermediaries. Thus, transactions can be carried out without having to share personal details with other third parties.

Financial Transactions/ Cryptocurrency

One of the better uses of a blockchain platform can also be for financial transactions. The majority of payments now are conducted through banks or financial institutions. If blockchains are used, lenders and borrowers can directly do so in an efficient, fast, and secure manner using cryptocurrencies which is a form of digital cash. This also makes the cost of blockchain transactions comparatively cheaper than bank transactions.

Charity

Blockchains can also be used to make donations visible, and share what the money is being used for in a charity. This has the potential to dramatically transform the charity industry by improving the trust of charitable stakeholders.

Resource: 25+ Essential Web 3.0 Terms You Need to Know to Understand It

Are there any disadvantages of Blockchain Technology?

As stated throughout this article, blockchain offers enhanced security, greater transparency, instant traceability, improved efficiency, and automation. However, there is some potential disadvantages of the technology that must be considered:

Slowed down process

While blockchains are inherently faster, they can potentially slow down processes if there are too many users in the network.

Scalability issues

The use of consensus algorithms and network congestions make blockchains hard to scale.

Inefficient

Since blockchains can potentially consume a lot of energy, they can be inefficient. This problem can be reduced by using private blockchain networks instead of public blockchain networks, but the entire problem cannot be solved.

Immutability can be an issue

Immutability can be an issue with blockchains especially if someone wants their information to be removed from the network. This can be a privacy issue.

Not completely secure

Blockchain by design is more secure than most networks, but there is still the issue of a 51% attack whereby if an entity can control more than 51% of the network, then security can be an issue. Blockchains can also be prone to DDoS attacks or cryptographic cracking (if the cryptography used is not secure enough).

Irrecoverable Keys

Peers use private keys to crack cryptographic hash in a block. If they forget the private key, they are forever locked out of the system, with no way to get back in. Not all peers/ users can be equally tech-savvy, and this can result in issues.

Costly

The cost of implementing blockchain initially is huge, and so are the maintenance costs associated with it.

Knowledge Requirement

Being a part of a blockchain network requires tech knowledge and proper training, which isn't always possible.

Interoperability issues

Most blockchains have their algorithms and solve problems their way, thus leading to interoperability issues when traditional systems use the technology.

Conclusion

In conclusion, the use of blockchain networks is becoming mainstream as we speak. While the technology does have its disadvantages, its use is becoming even more popular because of its verification efficiencies, security, enhanced visibility, and traceability.

In this day and time, it is hence extremely important for tech savvies to understand and become accustomed to the blockchain, as it seems like its use is only going to increase in the years to come.

Do not forget to check out what are the Top 10+ Blockchain Networks to look for in 2023!

References

Additional Web 3.0 & Blockchain articles to explore: